Property Tax Shortfalls are Common. Here’s how to Recover the Revenue.

July 19, 2022

Now That The Budget Is Over, Why Isn’t It Over?

October 18, 2022

Written by: Curtis L. Coonrod and Benjamin W. Roeger

If a city or town annexes territory, the county, and township lose revenue, right?

Yes, but maybe not as much as you might think. There are many misconceptions about what happens to local revenue when a city or town annexes territory.

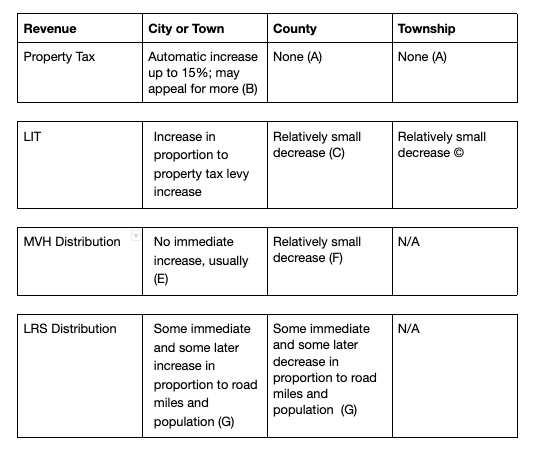

Here is a basic outline:

Effect of Annexation on Cities (or Towns), Countries, and Townships

(A) After annexation, the county and township may reduce their property tax levies voluntarily, but they are not required to do so.

(B) I.C. 6-1.1-18.5-12 and 13

(C) If the LIT distribution of any unit is increased, as usually happens when a city or town annexes territory, the increase to that unit is made up by a reduction that is shared by all the other units in the county. For example, if a county previously received 20% of all the LIT distribution in the county, and a city or town COIT or CAGIT distribution increases by $100,000, the county would lose up to $20,000. (A phase-in provision will protect the county from losing the full $20,000 in the first year.) Similarly, all the other cities, towns, and townships in the county would lose fractions of their distributions.

(D) It is a common misconception that the only township that experiences a LIT reduction is the township where the annexation takes place. That is wrong. The LIT distributions of all the townships and other civil units in the county are reduced proportionally. It does not matter in which township the annexation takes place.

(E) The MVH distribution to cities and towns comes from a different pool of gasoline tax revenue than the distribution to counties. It is based on population and is unaffected by the distribution to the county. Population increases are recognized only when there is a new census, every ten years. The exceptions would be if the city or town arranges for a special census or recertification. These take time and money, so normally the annexations result in no immediate increase.

(F) The MVH distribution to counties comes from a different pool of gasoline tax revenue than the distribution to cities and towns. Consequently, an increase to a city or town would have no direct impact on the distribution to the county. Each county receives a certain fixed distribution regardless of size; the rest of the county distribution is based on the number of vehicle registrations in the county and the number of county road miles. The latter factor is affected by annexation because road miles annexed by the city would no longer be considered county road miles.

(G) The LRS distribution is allocated within a county in proportion to road miles and population. Road miles would shift as a result of annexation, and the shift would normally take place within a year or two. The population would not change until a new census is taken. A special census or recertification of the census would increase the population of the city or town, and it would decrease the population of the unincorporated county.

*************

If you have questions or would like further information, please contact us at coonrod@coonrodcpa.com

This article is intended to provide information of general interest to local government officials in Indiana. The information is not guaranteed to be applicable or appropriate in particular circumstances. Local officials should consult competent professionals before acting on any information contained in this article. We are not attorneys. The advice of a legal nature should be sought only from qualified attorneys.

We inform you that any U.S. federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for (I) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing, or recommending to another party any transaction or matter addressed herein.

Copyright © 2022 C. L. Coonrod & Company